Covid Made Your Peloton Late

Covid Made Your Peloton Late

And will probably make it more expensive too

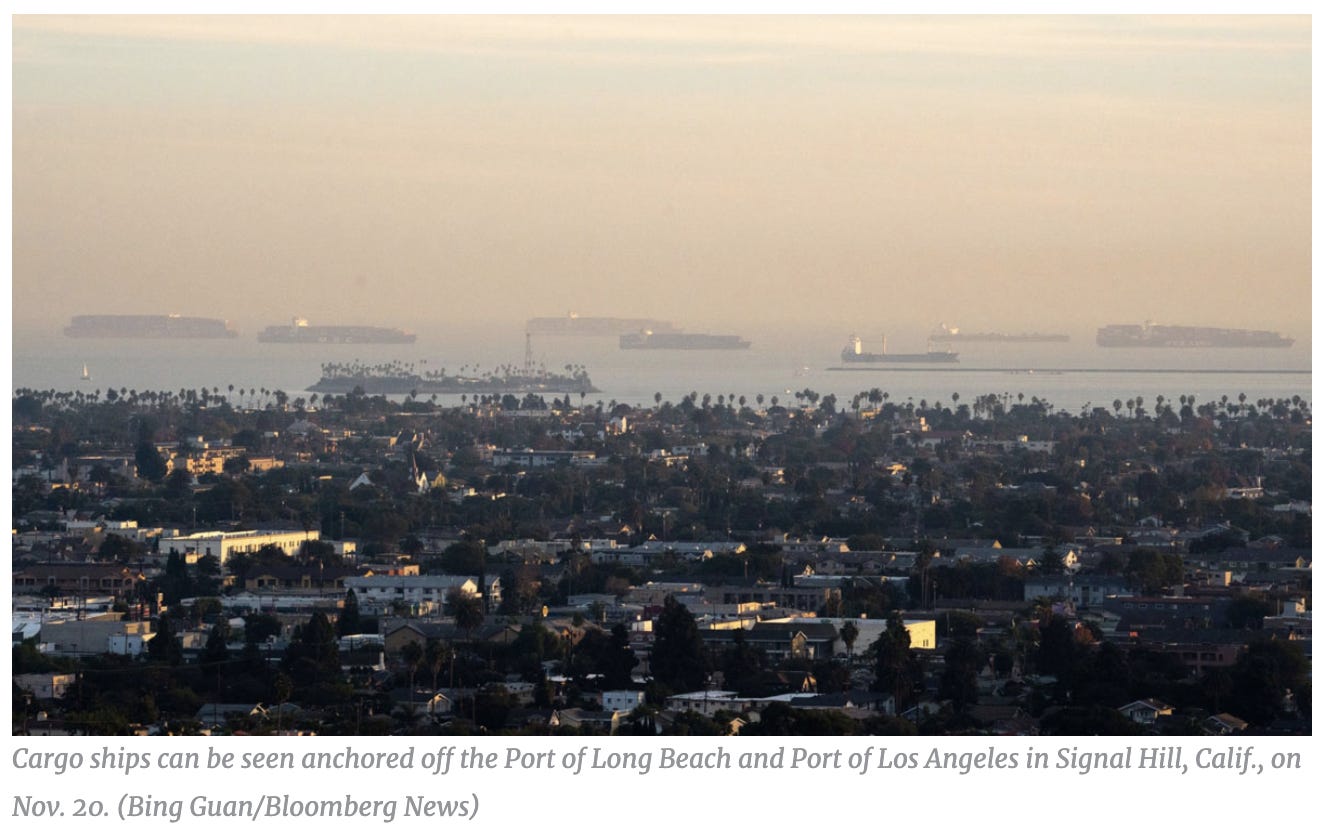

If you’re a Southern California surfer, you may have noticed something unusual in the water recently. Not sharks, not kelp, not toxic runoff - those are pretty normal. No, the weird objects in the water are dozens of massive cargo ships anchored in Santa Monica and San Pedro Bays. It turns out that just like with everything else, Covid-19 has ground the Southern California ports to a standstill.

And this in turn has started to have ripple effects across the entire US economy. Peloton’s stock recently cratered when it disclosed that delays are making it near-impossible to meet their production and delivery goals [The Verge]. Some of this is due to manufacturing delays, but some is due to the massive traffic jam in Southern California waters. Peloton is hardly alone either - this is increasingly affecting every seller of manufactured durable goods with production or supply chain in Asia, which is a whole lot of them. And it’s likely about to unleash chaos on US economic data.

The Key Role of SoCal Ports

Roughly 40% of American cargo traffic comes through the twin ports of Los Angeles and Long Beach [LAEDC]. Either would qualify as the largest in the United States by themselves and they’re literally next door to each other. The rise of China as a manufacturing center has supercharged the growth of these ports, and nowadays if you’re getting furniture, or auto parts, or paper goods, or a lot of other stuff they probably came from China via the ports of Los Angeles and Long Beach.

And over the fall and winter of 2020-2021, these ports have ground to a halt. Lengthy port delays at both the Port of Los Angeles and Port of Long Beach have meant that dozens of ships are currently anchored off shore waiting to unload [WSJ]. This, in turn, has meant that huge numbers of goods bound for the consumer market are currently trapped on board. Coupled with the huge pandemic-driven increase in demand for consumer durables - what housebound yuppie wants to go without a Peleton? - this has produced spiraling delays in all sorts of orders.

The crunch in consumer goods appears to be a perfect storm of Covid-driven supply shocks and Covid-driven demand shocks. On the supply side, there are two main shocks. The first is a shortage of the twenty-foot cargo containers, which is getting worse as so many are trapped in offshore waiting periods [CNBC]. The second is California’s pandemic, which is causing huge shortages in availability of highly skilled and hard-to-replace port personnel [WSJ]. On the demand side, there has been a spike in demand for consumer durables like exercise equipment and furniture [Brookings]. The result is rapidly escalating delays and skyrocketing shipping prices:

Break the world, break the datasets

If you’re a podcast listener, I highly recommend this episode of “Odd Lots” about the ongoing shipping crisis [Apple]. One of the most interesting insights is that Covid has sped up an already ongoing shift (sound familiar?) in the shipping industry, specifically away from the trend towards mega-container ships that can carry 10,000+ containers. While those megaships are more “efficient” in the sense of delivering lower unit costs for each container, they often carry hidden costs that only became obvious once they entered widespread use. The megaships require special ports which can easily become backed up, cannot fit in many narrow passages or canals, require special maintenance and fueling arrangements - all the hyper-specialized and ultimately brittle style of resource management that broke when Covid introduced large exogenous shocks into the environment.

The other fascinating macro-economic phenomenon is that intermediate economic agents seem to be responding to supply shocks with rationing and with delays rather than with increasing prices. For the most part, dealers of furniture and exercise equipment are not jacking up prices but are instead imposing lengthy wait times on consumers. This is surprising not just because increased prices would make it easier for them to meet their goals with less supply, but because the shipping delays are actually raising the sellers’ costs in a manner similar to tariffs [Transport Topics]. This is a case of what economists call “sticky nominal prices”: changing prices is annoying for businesses (it enrages customers, you have to rewrite billing codes, etc), so they generally try not to. If and when manufacturers finally decide to start raising prices en masse, this could take the form of a short, sharp shock!

Ultimately this chaos is a reminder that under extreme conditions like Covid, decision-makers in the policy or business world shouldn’t be looking at the data, but looking one level under the data. It would be a terrible mistake for the Federal Reserve to look at the (expected) sharp rise in outdoor dining or gasoline prices this summer as inflation run amok and stomp on the recovery. Thankfully, they have said they won’t be doing that [Reuters]. In the same vein, as I’ll write about in my next issue, economic data sets like the jobs report are going to be less reliable than in normal times.

Covid has broken the time series for everything, with shipping being no exception, and it’s not getting “fixed” for the foreseeable future. And so before making any decision based on data in 2021, it’s worthwhile now more than over to stop, take a beat, and ask whether the mapping of data to reality has changed.